International Insights Report

March 2026

Greater Phoenix’s economic relationship with the Asia-Pacific (APAC) region has deepened significantly in recent years. Driven by shifts in global supply chains, U.S. industrial trade and investment policy, and increased investment in advanced manufacturing operations, APAC partners represent critical trade, investment and workforce relationships across industries. This is especially true in semiconductors, in which Taiwan-centered partnerships have created one of North America’s most comprehensive production ecosystems, and batteries, in which LG Energy Solution committed $5.5 billion to a manufacturing facility in Queen Creek. These APAC connections provide a strong foundation for continued growth, even as policy volatility creates planning complexities for APAC-connected industries.

Trade

Arizona’s trade relationship with the APAC region reflects both the state’s deepening integration into global supply chains and its evolving economic diversification. While the APAC region accounts for 37% of total U.S. trade, Arizona maintains a higher concentration of its total trade at 47%.*

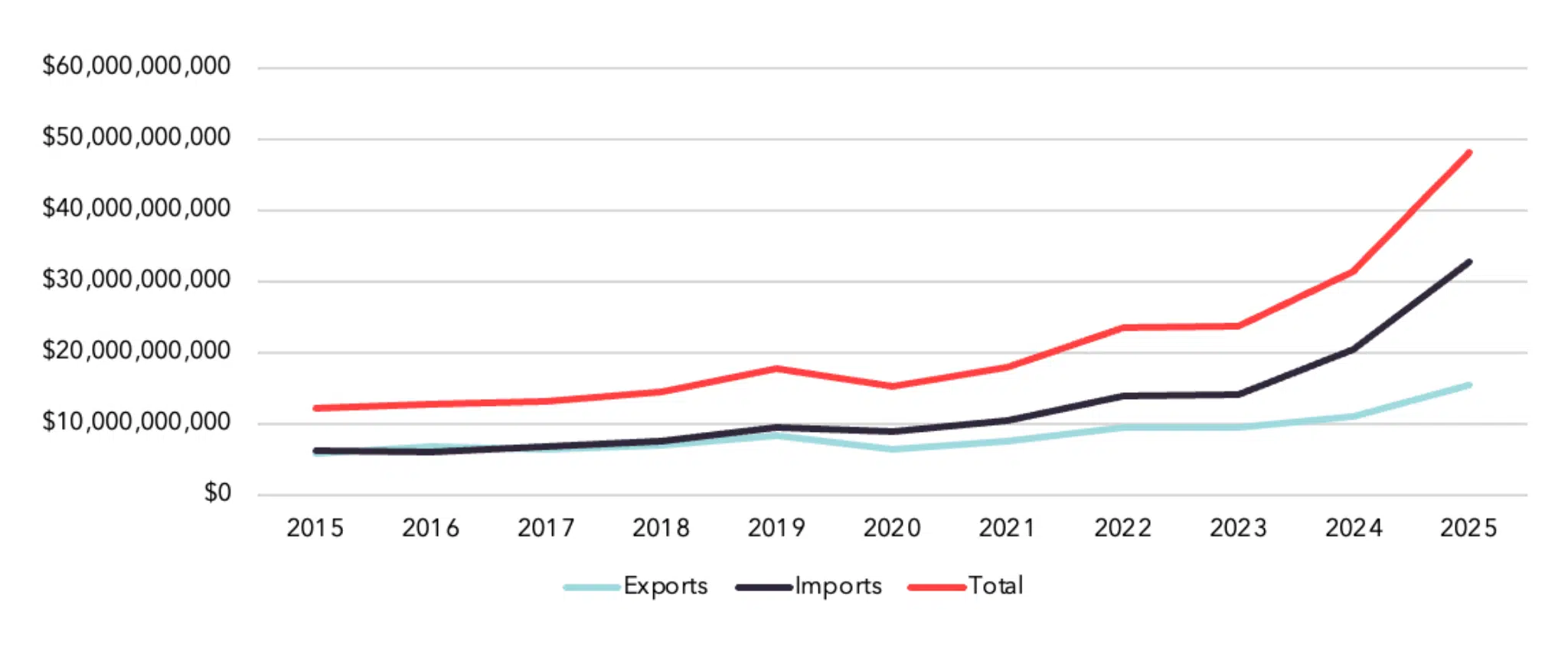

APAC trade has grown substantially over the past decade, primarily driven by increased imports over the past few years. Since 2015, Arizona’s APAC exports have more than doubled, while imports have grown more than fourfold.* This compares to more modest growth around 35% in both exports and imports between the U.S. and the APAC region overall, underscoring Arizona’s role as a high-growth connector between the APAC region and the western U.S.*

*Source: USA Trade Online, U.S. Census Bureau

2025 APAC Trade*

| Region | Exports | Imports | Total Trade | % of Total Trade Worldwide |

|---|---|---|---|---|

USA |

$637.50B |

$1,451.22B |

$2,088.72B |

37.3% |

Arizona |

$15,331.10M |

$32,820.13M |

$48,151.23M |

47.0% |

*Source: USA Trade Online, U.S. Census Bureau

AZ APAC Trade Over Time

Taiwan plays a significant role in Arizona trade. Currently, Taiwan is the second-largest market for Arizona exports and the largest source of imports to Arizona. Taiwan accounts for 44% of total APAC trade with Arizona.* This concentration reflects the state’s deep integration into Taiwan-centered semiconductor supply chains. Since 2020, Arizona’s exports to Taiwan have surged nearly 785%, from $514M to $4.5B, as semiconductor manufacturing output has grown, while imports of specialized equipment and materials have nearly doubled to $16.7B to support this production expansion.*

2025 Arizona Trade with Select APAC Countries*

| Country | Exports ($M) | Imports ($M) | Total Trade ($M) | Percent of APAC Trade |

|---|---|---|---|---|

Taiwan |

$4,547.12 |

$16,690.29 |

$21,237.41 |

44.1% |

China |

$1,563.25 |

$2,826.96 |

$4,390.20 |

9.1% |

Japan |

$1,440.23 |

$1,508.60 |

$2,948.83 |

6.1% |

South Korea |

$564.83 |

$1,768.12 |

$2,332.96 |

4.8% |

Singapore |

$1,143.21 |

$676.91 |

$1,820.13 |

3.8% |

India |

$780.09 |

$737.95 |

$1,518.05 |

3.1% |

Australia |

$522.39 |

$116.39 |

$638.79 |

1.3% |

*Source: USA Trade Online, U.S. Census Bureau

Greater Phoenix drives the majority of Arizona’s export activity to the APAC region. In 2024, Greater Phoenix exported $13.1B in goods to the region, representing a 40% increase from $9.4B in 2015.* This growth has been driven by expanding semiconductor and advanced manufacturing production, positioning Greater Phoenix as a critical node in trans-Pacific advanced manufacturing trade.

TSMC, which announced $165B of investment into Arizona, has been a catalyst for this growth.** Twenty-two Taiwanese projects have announced plans to join TSMC in the Greater Phoenix supply chain, which is expected to create at least 25,000 jobs.** Japan and South Korea have also emerged as key partners. Japan’s growth is driven by increased supplier activity from Intel and Amkor’s expansion, and South Korea is anchored by LG Energy Solution’s battery manufacturing facility. Japan leads with 17 foreign direct investment projects in 2025, while South Korea is establishing a smaller but growing presence with 4 projects and $5.7B investment since 2023.**

*Based on International Trade Association statistics for the Asia-Pacific Economic Cooperation (APEC) member countries

**Source: fDi Markets, Financial Times

Positions of Strength

The CHIPS Act accelerated transformative semiconductor investment in Greater Phoenix. With billions of dollars in federal grants to companies like TSMC, Intel and Amkor, the region has emerged as a primary U.S. hub for leading-edge semiconductor manufacturing and advanced packaging and testing. Government intervention continues to reshape America’s industrial landscape. Investment policies and incentives have shifted to trade policies that aims to continue the onshoring of critical industries. Given Greater Phoenix’s semiconductor industry’s deep integration with Asian supply chains, equipment manufacturers and technical expertise, this concentration has created a powerful draw for APAC partners looking to establish or expand U.S. operations. Government policies and customer demand also catalyzed a new segment of the semiconductor value chain to the region, such as Amkor’s $7B advanced packaging and testing facility under construction in Peoria, a first-of-its-kind project in the U.S.

This semiconductor ecosystem requires specialized workforce development, where Greater Phoenix demonstrates another key strength through its high-level coordination between all levels of higher education and industry leaders. At the community college level, programs like the Semiconductor Technician Quick Start program at Maricopa Community Colleges, and the Future48 Workforce Accelerator at Central Arizona College in partnership with LG Energy Solution train a talented workforce pipeline in critical industries. At the university level, Arizona State University’s Microelectronics Industry Council convenes industry partners and academic experts to collaborate on a unified vision for the regional semiconductor ecosystem. Grand Canyon University also partners with TSMC for an 11-week course that could end with a job offer. These initiatives create industry-led, customized training programs across multiple high-growth sectors.

Since 2015, APAC imports and exports through Phoenix Sky Harbor and Mesa Gateway airports have grown dramatically, with exports tripling and imports growing more than tenfold. Greater Phoenix’s direct air connectivity to the APAC region has strengthened in December 2025 and January 2026 with the launch of nonstop service to Taipei, reducing friction for executive travel, workforce collaboration, and supply chain management. These developments continue to enhance Phoenix Sky Harbor International Airport as the region’s primary global gateway, connecting Greater Phoenix to major international markets while driving economic activity across Arizona.

Challenges & Risks

The current administration’s aggressive trade policies, especially its use of tariffs, and the bilateral trade deals it is negotiating with other countries has intensified uncertainty as companies evaluate the impact of these policies on their business and investments. Policies including the evolving legality of implementation mechanisms impact the importation and exportation of goods, complicating near-term planning around supply chain configuration, pricing strategies and project timelines. While Greater Phoenix’s semiconductor sector benefits from explicit exemptions, the region faces particular exposure to the volatility given its concentration in semiconductors and advanced manufacturing, where supply chains, specialized materials and equipment are heavily sourced from overseas markets.

The fluid tariff environment extends decision-making cycles and fosters uncertainty, while stricter immigration policies impact cross-border workforce coordination. However, Greater Phoenix’s established position in semiconductor manufacturing and coordinated workforce infrastructure continues to attract strategic APAC investment in critical sectors.

Current Tariff Environment as of March 2026

Following a February 2026 Supreme Court decision invalidating emergency tariffs, the trade policy framework has undergone significant restructuring. While specific mechanisms continue to evolve, key elements affecting Greater Phoenix include:

- Section 122 tariffs announced after the Supreme Court decision establishes a 15% temporary global tariff that expires July 24th, 2026.

- Section 232 tariffs impacting steel, aluminum, copper, and automobiles and parts remain in effect.

- Semiconductor exemptions are in place for products relevant to the buildout of the domestic supply chain and manufacturing capacity.

- China tariffs from 2018-19 remain in effect under section 301, with new investigations announced for major trading partners.

Current Tariff Impacts on FDI Investment as of March 2026

- Bilateral, national investment commitments from Taiwan ($250B), Japan ($550B) and South Korea ($350B).

- These commitments, pending ongoing legal scrutiny, are expected to serve as catalysts for near-term APAC foreign direct investment.

Rapid industrial growth is placing increased pressure on water resources and energy infrastructure, which have become focal points around large-scale industrial projects. Water and energy infrastructure constraints have emerged as significant considerations for companies evaluating expansions throughout the U.S. As Arizona successfully addresses infrastructure prerequisites while managing timelines, approval processes, and resource availabilities and maintaining community support, it will sustain its long-term industrial growth.

Beyond tariffs and local infrastructure considerations, Greater Phoenix’s APAC-centered industries face external constraints outside regional control. Ongoing geopolitical uncertainty involving the Taiwan Strait represents persistent risk given the region’s deep integration with Taiwan-linked supply chains. Separately, uncertainty around immigration and visa policy constrains the mobility of specialized workers critical to semiconductor and advanced manufacturing sectors, complicating workforce planning for companies operating across borders.

Future Opportunities

Sustaining APAC‑linked growth will require a workforce that can scale. Competition for semiconductor and advanced manufacturing talent is global, placing pressure on regional training pipelines to keep pace with demand. While Arizona’s community college network has established comprehensive industry-aligned workforce training programs, extending similar coordination to K-12 education represents an emerging opportunity to strengthen the talent pipeline. Existing programs have proven that early exposure to advanced manufacturing careers through programs like West-MEC’s STEM Academy, East Valley Institute of Technology, and industry partnerships with schools like Hamilton High School can broaden awareness and interest in these pathways. However, some K-12 high school efforts remain at pilot scale compared to established community college infrastructure, suggesting there are opportunities for further development and expansion of primary and secondary education partnerships with advanced manufacturing industries.

Sky Harbor Airport acts as the region’s primary global gateway, connecting Greater Phoenix to major markets around the world while driving economic activity across Arizona. Meanwhile, the region’s secondary airport Mesa-Gateway is a growing cargo hub especially with DSV’s nearby new 950,000 square foot facility that will serve as its logistics hub. While the Taipei connection strengthens Greater Phoenix’s role as a gateway to Asia, expanding direct service to other major APAC markets like Japan, South Korea or even Australia, —a potential new market for sourcing critical minerals key to the region’s growing industries— would significantly enhance the region’s connectivity to Asian-Pacific markets and better position the region for further APAC investment.

Greater Phoenix’s connection with the APAC region remains in an early growth phase with significant potential for expansion. The semiconductor ecosystem that anchors current APAC relationships continues to show growth potential due to the scale of investments from Amkor, Intel and TSMC, growth of supplier networks, and maturing connection between APAC countries and Arizona. Looking ahead, the reindustrialization trend should continue as trade policies driven by national security and the need for supply chain resiliency compel onshoring.

Furthermore, the recently negotiated bilateral trade deals include investment commitments from key markets that may catalyze further investments in Arizona. Beyond semiconductors, aerospace and defense (A&D) represents a particularly promising frontier for APAC investment in Arizona. There is a growing number of A&D companies engaging with the region since 2024, suggesting this sector could emerge as the next wave of the Asia-Pacific partnership. Increased federal defense spending driven by heightened geopolitical tensions, may compel A&D manufacturers and suppliers from the APAC region to establish or expand U.S. operations, positioning Greater Phoenix well to capture this opportunity.

Download the PDF on Asia-Pacific Insights.

Industry Expert

Sean Fogarty

Vice President, International Business Development

Published: 03/24/2026